OCR Technology in Banking, What Actually Works (2026)

I have spent the last 18 months helping mid-market banks pick OCR vendors. Most marketing claims do not survive a real document set. Here is the unfiltered truth.

Table of contents

The most expensive sentence I have heard in banking technology was a community bank CFO telling me, "Our OCR vendor said 99% accuracy and we believed them." Three months later they had a $1.4M reconciliation backlog and a regulatory finding that started, "Failure to verify automated extraction outputs..." This guide is what I have learned helping mid-market banks pick OCR vendors over the last 18 months. The version where vendor demos do not survive contact with real documents.

If you are evaluating OCR for a bank, community, regional, or BaaS sponsor, read this before you sign anything.

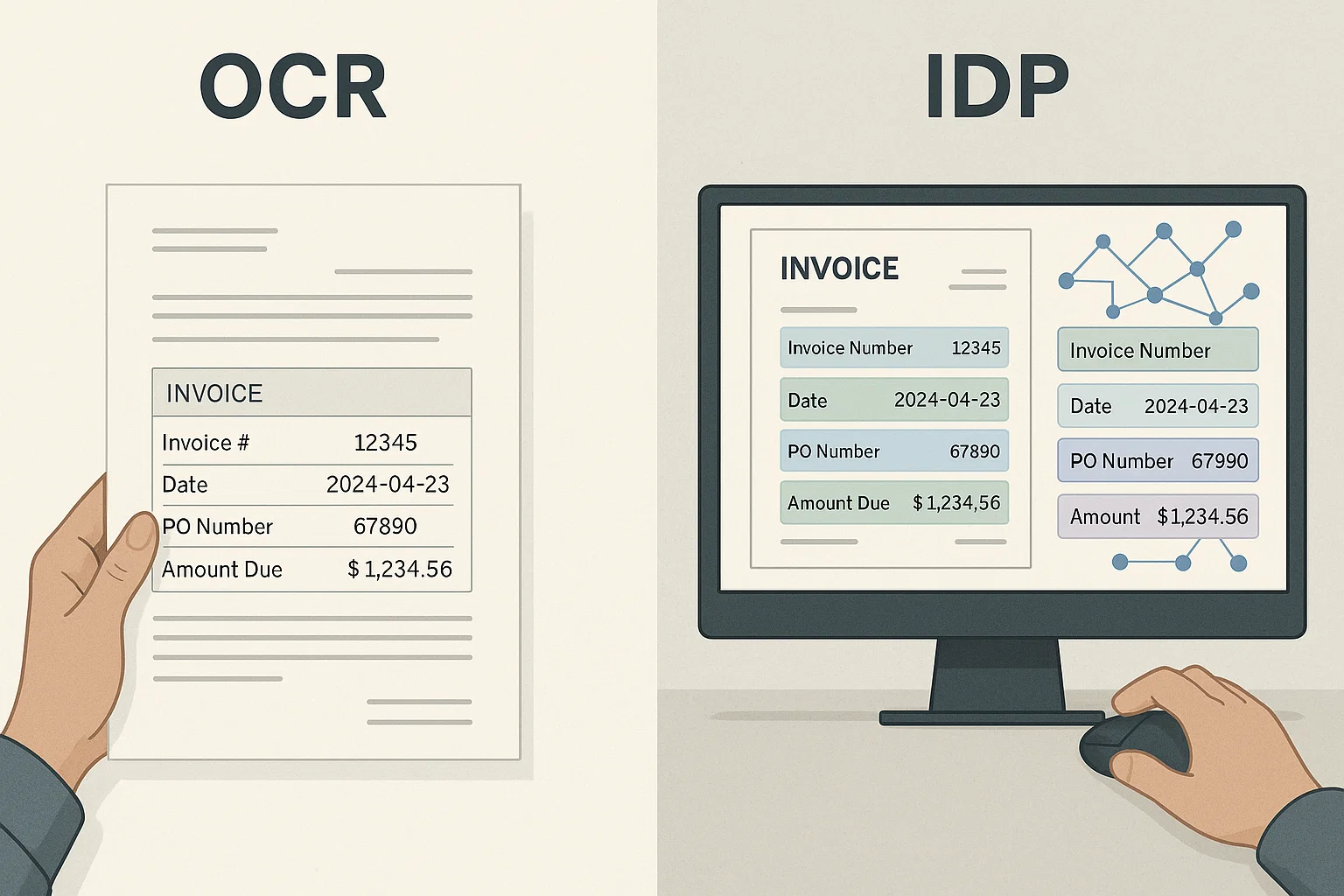

What "OCR Technology in Banking" Actually Means

OCR (Optical Character Recognition) in banking is the use of software to read pictures of documents, bank statements, deposit slips, loan applications, KYC IDs, wire instructions, mortgage packets, and turn them into structured data your core banking or BSA system can use. The friendly description: a tireless junior employee who types extracted data into your systems at a penny per page and never gets bored.

The unfriendly reality: banking is a regulated industry with audit trails, customer privacy obligations, and consequences for errors that other industries do not face. OCR that works for a marketing agency may not survive an OCC examination. This is the gap most vendor pitches paper over.

For a foundational explanation of OCR itself, our optical character reader 2026 piece is the simpler starting point. Come back here when you need the banking-specific lens.

The Five Banking Workflows OCR Actually Helps

1. Loan Application Document Intake

The biggest single time sink in commercial and SBA lending is the document intake step. Customers send PDFs, photos, scans, and emails. Before any underwriting can start, someone has to extract the relevant data. OCR cuts this step from days to minutes. Modern OCR APIs handle bank statements, tax returns, business licenses, and ID documents in one pipeline.

Our automated bank statement analysis guide goes deep on this.

2. KYC and Onboarding

Customer onboarding requires identity verification documents, driver's licenses, passports, utility bills. OCR plus liveness detection drops onboarding time from days to seconds. Regulators expect documented audit trails, which good OCR APIs provide by default.

The KYC document verification piece covers what auditors actually look for.

3. Check Processing

Paper checks are not going away as fast as anyone predicted. OCR for checks reads the MICR line, courtesy amount, and legal amount, then validates them against each other to catch fraud. Most modern banks already have this; what changes in 2026 is the integration with downstream fraud detection.

4. Wire and Payment Instruction Processing

SWIFT messages, ACH instructions, and wire transfer forms all contain structured fields. OCR extracts sender, recipient, amount, currency, and purpose. Combined with sanctions screening and OFAC checks, this becomes an automated payment review pipeline. Our AML document checks piece covers the seven-field minimum.

5. Mortgage Origination Document Review

Mortgage packets are 300-500 pages of mixed documents, pay stubs, tax returns, bank statements, property appraisals, insurance binders, employment verification letters. Without OCR, a mortgage processor spends 8-12 hours on document review per file. With OCR and intelligent classification, that drops to 2-3 hours.

The Vendor Demo Tells

Every vendor demo I have sat through follows the same structure. Slide 1: a beautiful invoice. Slide 2: a 98% accuracy claim. Slide 3: a multi-million dollar customer case study. Your real documents look nothing like slide 1. Here is what to test instead.

Test 1: Your Worst Customer Document

Pick the most messy document from your last 50 onboarding cases. Phone photo. Faded scan. Wrinkled paper. Run it through the demo. If the vendor refuses, you have your answer.

Test 2: Multi-Page Tables

A 12-page bank statement with a transaction table spanning all 12 pages. Naive OCR treats each page as a separate table. The demo should produce one logical table with all transactions in order.

Test 3: Mixed Languages

If you serve any non-English-speaking customers, test a document with mixed scripts. English form fields with Mandarin signatures, for example. Many OCR engines silently fail here.

Test 4: A Handwritten Signature Over Text

A common real-world case: an applicant's handwritten signature partially covers a typed dollar amount. Good OCR reads the underlying text correctly. Bad OCR returns hash or skips the field.

Test 5: A Document with No Header

Some banks receive scanned packets without obvious page breaks or document boundaries. Good systems segment the packet into individual documents automatically. Bad ones treat the whole packet as one document and produce useless output.

What Regulators Care About

The OCR vendor will not bring this up. You should:

1. Data Residency

Where does the document live during processing? If it leaves the US for any part of the pipeline, you have a regulatory disclosure obligation for some customer types. Pick a vendor with US-only data residency.

2. Retention Policy

How long does the vendor store documents after processing? Anything over 24 hours is a flag. Best practice: vendor deletes within 1 hour of successful response.

3. Audit Trail

Can you reconstruct, for any given extracted field, what document it came from, what time it was processed, what confidence score the OCR assigned, and who reviewed it if confidence was low? Regulators expect all four.

4. Model Training

Does the vendor train its models on your data? Many cheap OCR services do. For regulated workflows, require a written "no training on customer data" clause.

5. SOC 2 Type II

SOC 2 Type I is a snapshot. Type II is an evidence-based audit over 6-12 months. For banking workloads, require Type II reports under NDA.

The Pipeline That Passes OCC Examinations

Across the bank OCR rollouts I have observed pass clean OCC and FDIC reviews, the pipeline shape is consistent:

- Capture, document arrives via email, portal, or API

- Validate file integrity, magic-byte check, virus scan, size limits

- Classify, what type of document is this?

- Pre-process, deskew, rotation correction, page boundary detection (see our document detection guide)

- OCR, layout-aware extraction

- Field extraction, pull the fields specific to that document type

- Normalize, date formats, currency, account number patterns

- Validate, checksums, format rules, cross-field consistency

- Screen, sanctions lists, PEP lists, internal fraud flags

- Log everything, immutable audit trail with timestamps and operator IDs

- Route exceptions, low-confidence extractions go to a human queue with the suspect fields highlighted

- Push to downstream, core banking, loan origination, BSA monitoring

Each step is small. Together they survive audits.

What Free OCR Cannot Do for a Bank

Free tools like Tesseract, ocrmypdf, or Google Drive's hidden OCR are wonderful for personal use. They are not appropriate for banking workflows because they lack:

- Documented data residency guarantees

- SOC 2 reports

- BAAs for any healthcare-adjacent flows

- Retention policies you can audit

- Layout-aware extraction for multi-page tables

- Sanctions and fraud screening hooks

- Field-level confidence scores for exception routing

You can build all of this on top of Tesseract. It takes 6-9 months and a small team. Most banks buy.

OCR cost in banking by institution size

OCR economics in banking scale non-linearly with institution size because the fixed costs (integration, compliance validation, exception queue tooling) amortize differently across document volume. A community bank processing 5,000 documents/month and a regional bank processing 500,000 face completely different buy-vs-build math. Here's the honest breakdown by bank tier.

| Bank tier | Monthly doc volume | Recommended approach | Annual cost range |

|---|---|---|---|

| Community (<$1B assets) | 2K-15K | Single vendor, US data residency, SOC 2 Type II | $30K-$120K |

| Regional ($1-10B) | 50K-300K | Core OCR for routine + specialty vendor for complex packets | $150K-$600K |

| Regional ($10-50B) | 300K-1M | Multi-vendor + partial in-house pipeline | $600K-$2M |

| Large ($50B+) | 1M+ | In-house pipeline on builder OCR APIs | Custom (build economics) |

The cost-per-document at the community-bank tier ($0.50-$2.00 fully loaded including compliance overhead) is much higher than the large-bank tier ($0.05-$0.15) precisely because compliance and integration costs don't shrink with volume. This is why community banks should never build, the fixed compliance-validation cost alone (SOC 2 review, examiner documentation, audit-trail tooling) exceeds a year of vendor fees.

The banking regulatory landscape for OCR in 2026

Banking OCR sits inside a regulatory framework that other industries don't face, and the specific regulators and rules determine what your OCR pipeline must document. Understanding this landscape before vendor selection prevents the "we bought OCR and then failed the exam" outcome that opened this article.

The regulators and what each cares about

The OCC (national banks) and FDIC (state non-member banks) examine model risk management, for OCR, that means documented validation that extraction outputs are verified, not blindly trusted. The Federal Reserve layers on SR 11-7 model risk guidance, which increasingly gets applied to ML-based extraction. FinCEN governs the BSA/AML side, any OCR feeding transaction monitoring or KYC must produce audit trails that support SAR filings. The CFPB cares about fair-lending implications when OCR feeds credit decisions (ECOA adverse-action documentation). State regulators add their own requirements, especially for money transmitters and BaaS sponsors.

The four documentation artifacts examiners request

Across the clean exams I've observed, examiners consistently request four artifacts for OCR-driven workflows: (1) the model validation report showing extraction accuracy was tested on representative documents, (2) the exception-handling procedure showing low-confidence extractions get human review, (3) the audit trail demonstrating per-field traceability from source document to system-of-record, and (4) the vendor due-diligence file including SOC 2 Type II and the no-training-on-customer-data clause. Have all four ready before the exam, not during it.

Real deployment: a $3B regional bank's mortgage OCR rollout

In Q4 2025 I helped a $3B-asset regional bank deploy OCR for mortgage origination document review. Starting state: mortgage processors spent 8-12 hours per file on document review across 300-500 page packets, processing ~180 mortgages/month, with a 34-day average time-to-close that was losing them deals to faster competitors.

The deployment: DocsAPI for OCR + classification (segmenting the packet into pay stubs, tax returns, bank statements, appraisals, title docs), a custom validation layer checking income figures across documents for consistency, and an exception queue for anything below 95% confidence. The compliance work, model validation report, examiner documentation, audit-trail tooling, took as long as the engineering (10 weeks each, run in parallel). Post-deployment: document review dropped from 8-12 hours to 2-3 hours per file, time-to-close fell to 19 days, monthly volume grew to 240 mortgages with the same processing team. The bank passed its next OCC exam with no OCR-related findings because the four documentation artifacts were ready. For the mortgage-specific depth, see our mortgage OCR field manual.

The Way I Explain Banking OCR to a Branch Manager

Imagine you hire a careful, patient employee whose only job is to read paperwork and type the important parts into your systems. She does not make mistakes on dollar amounts. She does not get tired in the afternoon. She works for less than a penny per page. The only thing she cannot do is decide whether to approve a loan or flag a transaction as suspicious. That is your job.

OCR in banking is that employee. The bank is still the bank. The decisions are still yours. The paperwork just stops being the bottleneck.

What I'd Do Today

If you are at a community bank under $1B in assets: do not build your own OCR. Pick a vendor with proven banking customers, real SOC 2, and clear US data residency. Use the five tests above.

If you are at a regional bank ($1-50B): you need a multi-vendor strategy. Use your core's built-in OCR for routine documents. Layer a specialty vendor for mortgage, KYC, or commercial lending packets where the core's OCR falls short.

If you are at a BaaS sponsor: your liability profile is higher than your customers expect. Require your fintech partners to use OCR vendors you have approved. Audit their extraction logs quarterly. (I write about these regulated-industry tradeoffs often.)

Frequently Asked Questions

What is OCR in banking?

OCR in banking is software that reads pictures of banking documents, statements, applications, IDs, wire instructions, and turns them into structured data for core banking, loan origination, and BSA systems.

How accurate does OCR need to be for banking?

For automated decisions, regulators generally expect 99%+ accuracy on critical fields with documented validation. Below 99%, the workflow needs a human review queue for low-confidence extractions. The exact thresholds vary by regulator and product.

Can OCR alone meet BSA/AML requirements?

No. OCR extracts data; meeting BSA/AML requires the extracted data to flow into a monitoring system with SAR-generation capability, sanctions screening, and immutable audit trails. OCR is one component, not the whole compliance stack.

What banking documents are hardest for OCR?

Handwritten check stubs, faded multi-generation photocopies, packets without page boundaries, and any document with stamps or signatures over critical text fields. Modern engines handle 90-95% of these correctly with proper pre-processing.

Should banks build or buy OCR?

For meaningful volume above 10,000 documents per month, build-versus-buy depends on engineering capacity. Most community and regional banks should buy. Most large banks have already built. The middle ground (regional banks) is where the hardest decision lives.

How much does OCR cost in banking?

Per-page pricing typically runs $0.02-$0.10 depending on document complexity and features (classification, validation, screening). At meaningful volume, expect 60-80% cost reduction compared to manual processing within 6-12 months.

Frequently asked questions

OCR in banking is software that reads pictures of banking documents, statements, applications, IDs, wire instructions, and turns them into structured data for core banking, loan origination, and BSA systems.

For automated decisions, regulators generally expect 99%+ accuracy on critical fields with documented validation. Below 99%, the workflow needs a human review queue for low-confidence extractions.

No. OCR extracts data; meeting BSA/AML requires the extracted data to flow into a monitoring system with SAR-generation capability, sanctions screening, and immutable audit trails. OCR is one component.

Handwritten check stubs, faded multi-generation photocopies, packets without page boundaries, and any document with stamps or signatures over critical text fields. Modern engines handle 90-95% with proper pre-processing.

For meaningful volume above 10,000 documents per month, build-versus-buy depends on engineering capacity. Most community and regional banks should buy. Most large banks have already built.

Per-page pricing typically runs $0.02-$0.10 depending on document complexity and features. At meaningful volume, expect 60-80% cost reduction vs. manual processing within 6-12 months.

Related Blog Posts

How to Make a PDF Searchable in 30 Seconds (No Acrobat)

Your PDF won't let you search inside it? Here is the 30-second fix, the four traps that silently break it, and a simple kid-friendly explanation of what's actually happening.

Readable PDF vs Image PDF: How to Tell the Difference Fast

Your PDF looks normal but Ctrl+F finds nothing. That means it is an image PDF, not a readable one. Here is the 2-second test and the simple fix.

OCR a PDF: 4M-Pages-a-Month Lessons From Production (2026)

Everything I learned running OCR on 4 million PDF pages a month, what breaks, what works, and the engineering corners marketing decks always skip.

Ready to Transform Your Lending Process?

See how DocsAPI's AI-powered industry classification can help you process loans faster, improve accuracy, and scale your operations.